Alpha Lives in the Tails

Betting on Non-Consensus, and Finding Mispriced Assets

One of the tensions every venture capital manager feels is:

How do I remain disciplined to my thesis and entry price?

How do I not miss truly asymmetric venture-scale outliers?

I always say in the short run discipline matters, but in the long run your job as a venture capitalist is provide accretive capital to unseen opportunities that pre-date market consensus, and that in turn, will afford you outlier performance and make your limited partners money. Asymmetries in returns come from two things:

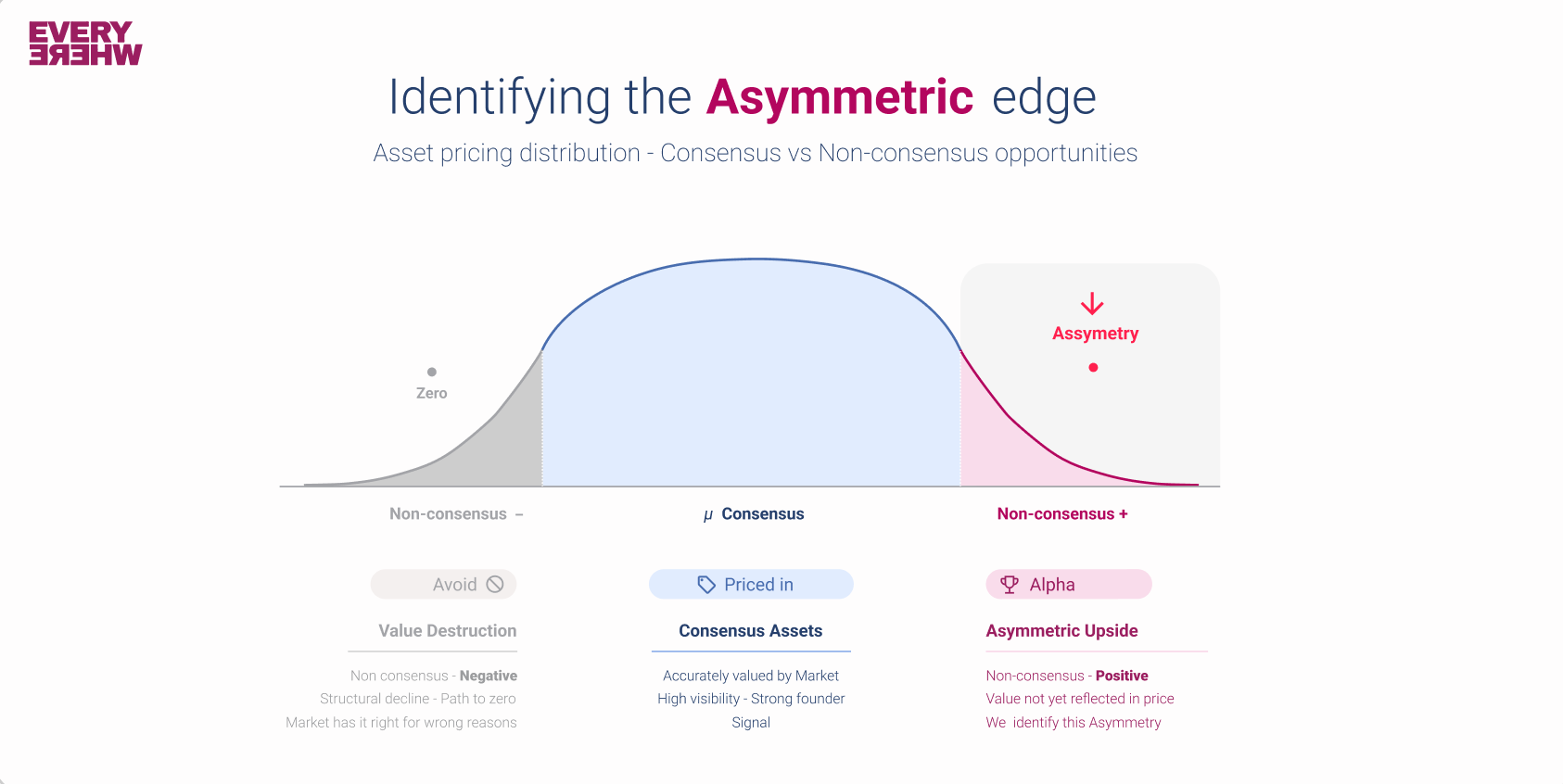

Finding consensus before the market

Harvesting under-priced assets, where price < intrinsic value

One empirical observation we’ve had at Everywhere Ventures over the last 8 years, and I saw during my prior 7 years investing at Mohr Davidow Ventures and founding Two Culture Capital, was that our biggest outliers were always “in the tails.” They were in the periphery of what we said that we did. “We don’t do consumer,” but we were the first check into Pair Eyewear, which has gone up 100x since we invested. “Markets like Algeria are too small,” but we returned 100x on Yassir when it became the Super App of Francophone Africa, and the Maghreb. “Hardware is hard,” but we saw Umbra build Synthetic Aperture Radar (SAR) satellites and catapult to a billion dollar valuation and massive profitability. “Data centers in space is a crazy idea,” but as cost per kilogram continues to fall with SpaceX, Benchmark validated our early bet by marking up that position 100x and turning Starcloud into a unicorn in 17 months, the fastest ever in Y-Combinator history. When we pre-seeded Headway in 2018 many presumed mental health wasn’t a big enough market. Andreessen led their last round at over $2.4 billion. My co-founder Jenny Fielding pre-seeded Chainalysis at Techstars when web3 wasn’t yet on the map. Today Accel and GIC value it at $8.6 billion.

Part of investing in the tails is that firms operate on conviction. Generally to do something truly out of the box, one partner on the team has to feel it viscerally, be unable to sleep, keep bringing up the idea at partner meetings until the rest of the team eye rolls and says “ok fine, if you love it so much you should just do it!”

Every deal requires a “burden of proof” to get done. Diligence. Calls with customers. Reference checks on the team, the cap table, the co-investors. But when one partner is going farther out into the tail, that burden of proof has to go up. You have to prove with unreasonable conviction that you want to make the investment anyway. Despite convention, despite disagreement, despite consensus opposition. Great deals are not lukewarm, they are polarizing. And if you’re an entrepreneur and some people don’t absolutely hate your idea, or think you’re crazy, you’re not swinging big enough.

The second truth today is that venture capital is no longer a cottage industry like it was when I was a kid in Palo Alto, when soccer dads played with Palm Pilots and talked about personal computing and the rise of DotCom opportunities. Back then there were 20 firms on the map, and there was not a glut of capital chasing the same opportunities. The frontier of the "tail” moves. The Internet was a tail bet in the mid 1990s. The social web was a tail bet in the mid aughts. SaaS was a tail bet in the early teens. Crypto was a tail bet in the late teens. Perhaps space is a tail bet today.

What’s clear is that frameworks lag reality, as I’ve written about before. Heuristics of what worked last year are most certainly NOT what will work this year. Part of this means that a glut of capital is chasing a lagging consensus, and therefore any potential alpha is “priced in.” When I called my friend Clay Bavor when he started Sierra AI, he said “sure write a check, but Sequoia’s doing it at a billion.” Clay and Bret Taylor are exceptional, and Sequoia was already pricing in value at a billion. There is still certainly alpha in that company, as it’s a rising AI juggernaut, but that’s not the game we play at Everywhere Ventures. We’re primarily investing outside the Valley, and looking for asymmetries in the tails, and mis-priced assets, where there are undiscovered, yet exceptional founders, who have a mismatch of price to value.

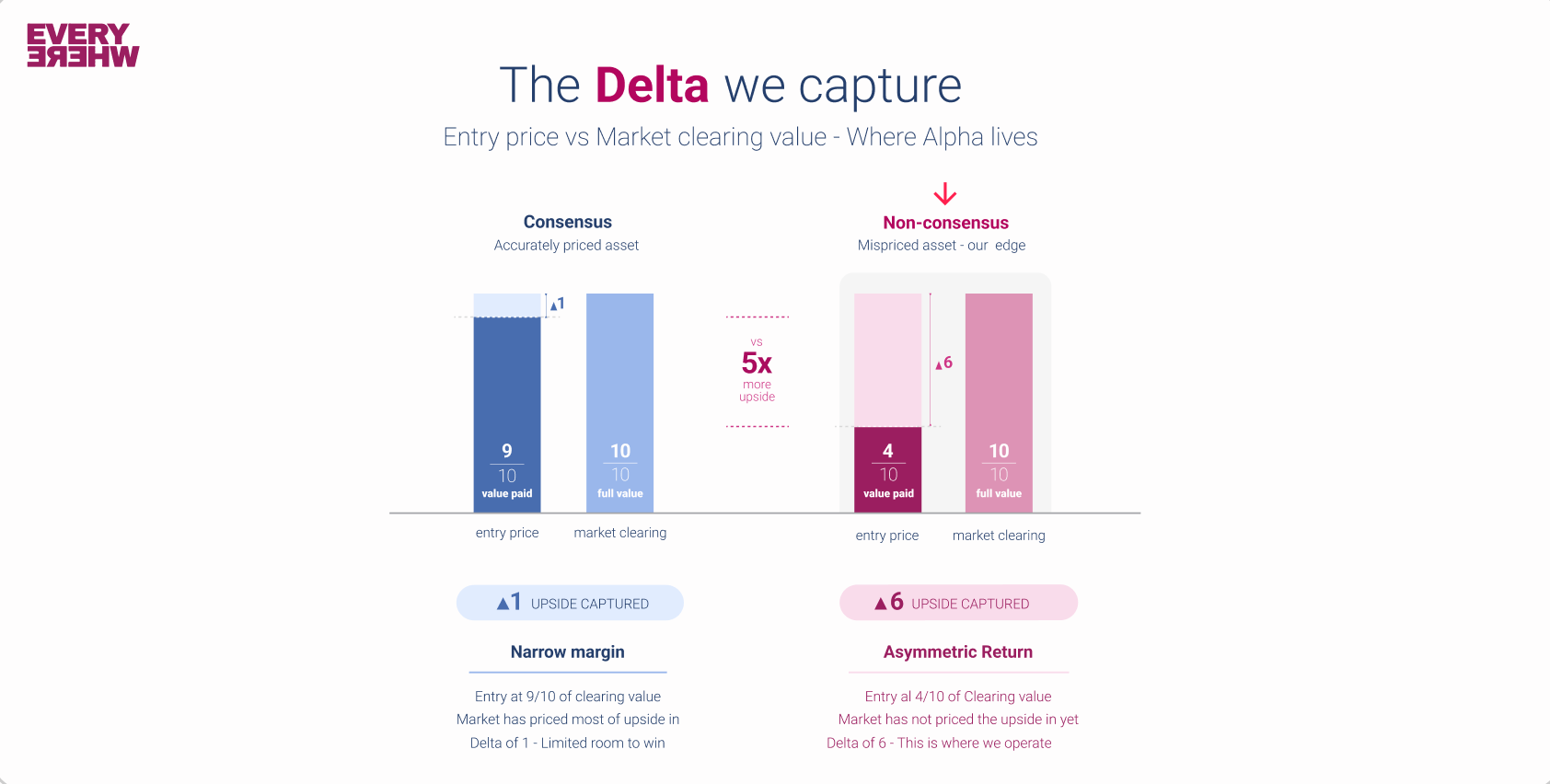

In a consensus deal value is priced in. In the example above, the price may be nine, but the value is ten. The value capture to the investor is one. Outside of key industries, in first-time rounders, and in remote geographies, the delta between price and value is higher. In non-consensus deals (for the above reasons) price may be four when value can still be ten. This delta of six is the potential non-consensus upside, the alpha.

At Everywhere Ventures we ourselves are a non-consensus firm. We’re bicoastal, we’re very early pre-seed, we primarily invest outside of the Bay Area gold rush. But what we believe is that our network of 1,000 founders as LPs and portfolio CEOs give us unfair access into these tails via compounding network effects in venture capital. And because we constantly evaluate “where the tail is,” whether sector, geography, or founder archetype, we’re focused on finding these mis-priced assets in the market. We write three times more checks than firms our size, and we return capital. We’ve charted to the top decile every fund, every cohort, every year for the last decade.

Venture capital is an evolving game, but the lessons above hold true. Always.

—

Scott Hartley is Co-Founder & Managing Partner of Everywhere Ventures. Special thanks to Michael Barone and Amelia Muro Garlot for support on this post.